Nuclear Power in South Africa

- South Africa has two nuclear reactors generating 5% of its electricity.

- South Africa's first commercial nuclear power reactor began operating in 1984.

- Electricity supply is unreliable, with businesses and households facing frequent rolling blackouts.

- Government commitment to the future of nuclear energy has been strong, but financial constraints are severe.

- In January 2024 the government published plans to procure 2.5 GWe of new nuclear capacity. However in August 2024 the government paused the process to allow for further public consultation.

- The country’s latest resource plan outlines 5.2 GW of new nuclear capacity to be online by 2039.

Reactors

Construction

Shutdown

Operable nuclear capacity

Electricity sector

Total generation (in 2023): 229 TWh

Generation mix: coal 187 TWh (82%); wind 11.6 TWh (5%); nuclear 8.5 TWh (4%); oil 8.1 TWh (4%); solar 6.8 TWh (3%); hydro 6.7 TWh (3%); biofuels & waste 0.5 TWh.

Import/export balance: 0.5 TWh net export (10.7 TWh imports; 11.3 TWh exports)

Total consumption: 185 TWh

Per capita consumption: c. 2900 kWh in 2023

Source: International Energy Agency and The World Bank. Data for year 2023.

Electricity consumption in South Africa has been growing rapidly since 1980 and the country is part of the Southern African Power Pool (SAPP), with extensive interconnections. Total installed operating capacity in the SAPP countries is about 67 GWe, of which 75% is South African, mostly coal-fired, and largely under the control of the state utility Eskom.

Eskom supplies about 90% of South Africa's electricity and about 30% of the electricity produced in Africa. Eskom's installed capacity was 53.0 GWe as of July 2025 (excluding wind and small-scale hydro), of which coal-fired stations accounted for about 45.3 GWe.

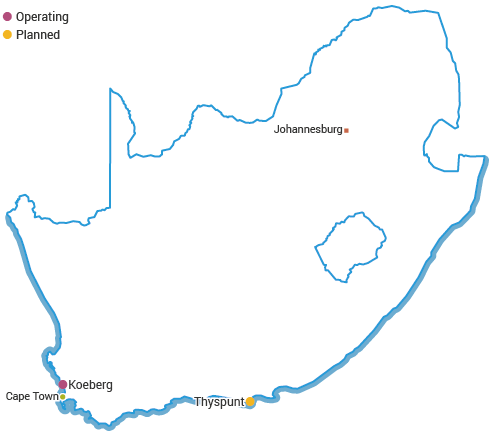

South Africa's main coal reserves are concentrated in Mpumalanga in the northeast, while much of the load is on the coast near Cape Town and Durban. Moving either coal or electricity long distance is inefficient, so it was decided in the mid-1970s to build some 1800 MWe of nuclear capacity at Koeberg near Cape Town.

Nuclear power industry

Operable reactors in South Africa

The South African nuclear industry dates back to the mid-1940s, when the predecessor organization to the Atomic Energy Corporation (AEC) was formeda. In 1959, the government approved the creation of a domestic nuclear industry and planning began the next year on building a research reactor, in cooperation with the US Atoms for Peace programme. The Pelindaba site near Pretoria was established in 1961, and the 20 MWt Safari-1 reactor there went critical in 1965b.

The Koeberg plant was built by Framatome and commissioned in 1984-85. It is owned and operated by Eskom and has twin 900 MWe class (970 & 940 MWe gross) pressurized water reactors (PWRs), the same as those providing most of France's electricity. Stress tests similar to those in the EU were carried out in 2011 with International Atomic Energy Agency (IAEA) help.

Both units have undergone major upgrade work, including replacement of steam generators, to extend their operating lives by 20 years. Eskom awarded the contract for the six replacement generators to Areva (now Framatome), despite protests from Westinghouse. They were manufactured under subcontract by Shanghai Electric Nuclear Power Equipment Company (SENPEC). As part of the lifetime extension work the secondary turbine systems were upgraded by Jacobs Engineering, boosting capacity by about 10%.

South Africa has insufficient electricity generation capacity. In February 2023 President Cyril Ramaphosa declared a national 'state of disaster' to tackle the electricity crisis in the country. The declaration enabled the government to take practical measures to address the economic damage caused by debilitating electricity shortages. With Koeberg 1 being offline, along with the extended outage of three units at the Kusile coal-fired power station, South Africa's power system was severely constrained in mid-2023.

The first steam generator was removed from unit 1 in March 2023, after the unit entered a refuelling and maintenance outage in December 2022. Unit 1 had been expected to remain out of service until June 2023, but in August 2023 a five-month delay to the ongoing steam generator replacement campaign was announced due to schedule complications and logistical issues. Koeberg 1 restarted in November 2023. In July 2024 the regulator granted Eskom a 20-year licence extension for unit 1, allowing it to operate until 21 July 2044.

Koeberg 2 was taken offline for its maintenance outage and steam generator replacement in December 2023. It returned to service a year later, in December 2024. In November 2025 the regulator granted Eskom a 20-year licence extension for unit 2, allowing it to operate until November 2045.

Earlier, in September 2023 KEPCO signed an agreement with Eskom to perform maintenance at the Koeberg plant. Starting in October 2023, the maintenance was expected to take over three years and cost around $640 million.

Further nuclear capacity

In 2006 the government of South Africa announced that it was considering building a further conventional nuclear plant, possibly at Koeberg, to boost supplies in the Cape province. Since then, numerous proposals have been put forward for new capacity, as outlined below.

In early 2007, the Eskom board approved a plan to double generating capacity to 80 GWe by 2025, including construction of 20 GWe of new nuclear capacity so that nuclear contribution to power would rise from 5% to more than 25% and coal's contribution would fall from 87% to below 70%. The new programme was to start with up to 4 GWe of PWR capacity to be built from about 2010, with the first unit commissioned in 2016. The environmental assessment process for the so-called 'Nuclear-1' project considering five sites, and selection of technology was to follow in 2008. Areva's (now Framatome's) EPR and Westinghouse's AP1000 were short-listed. Areva headed a consortium of South African engineering group Aveng, the French construction group Bouygues and EDF which submitted a bid to supply two 1600 MWe EPR units. Westinghouse matched this with a bid of three 1134 MWe AP1000 units. The Westinghouse-led consortium included The Shaw Group and the South African engineering firm Murray & Roberts.

Areva and Westinghouse also offered to build the full 20 GWe – with a further ten large EPR units or 17 AP1000 units by 2025. This would have been coupled with wider assistance for the local nuclear industry, in the Westinghouse case including development of the Pebble Bed Modular Reactor (Westinghouse was an investor in the PBMR company and was then sponsoring the design in the USA – see section on PBMR below). However, in December 2008, Eskom announced that it would not proceed with either of the bids from Areva and Westinghouse, due to lack of finance, and the government then confirmed a delay of several years2.

In IRP 2010, nuclear prospects were revived, for 9600 MWe, supplying 23% of the electricity. In November 2011 the National Nuclear Energy Executive Coordination Committee (NNEECC) was established as the authority for decision-making, monitoring, and general oversight of the nuclear energy expansion program. An IAEA integrated nuclear infrastructure review (INIR) was carried out in 2013.

Although IRP 2010 included six new 1600 MWe reactors coming online in 18-month intervals from 2023, Eskom said that it would be looking for lower-cost options than the earlier AP1000 or EPR proposals, and would consider Generation II designs from China (perhaps CPR-1000) or South Korea (perhaps OPR). The capital cost per installed MWe of a CPR-1000 was said to be about half that of an AP1000 or EPR.

Early in 2011 Areva stepped up its involvement with the Nuclear Energy Corporation of South Africa (Necsa), and early in 2013 Rosatom declared its interest in bidding. Bids were expected to be called early in 2014 so that the contractor/vendor could be on site in 2016, with a view to 2023 operation of the first unit. Initially about 30% local content was expected in the project, rising to 40% later.

In October 2013 Westinghouse signed an agreement with the Sebata Group of engineering companies to prepare for 'potential construction' of new nuclear plants in South Africa.

In November 2013 Necsa signed a broad agreement with Russia's NIAEP-Atomstroyexport and its subsidiary Nukem Technologies, to develop a strategic partnership including nuclear power plants and waste management, with financial assistance from Russia. It is uncertain just what this means, but Rosatom said that it “offers South Africa to build the entire process chain of nuclear power plant construction and operation.” “The strategic partnership implies joint implementation of the national nuclear power development program of South Africa. The key project is construction of new nuclear power plants with the Russian VVER reactors totalling 9.6 GW (up to eight power units) in South Africa."

In September 2014 Rosatom signed an agreement with South Africa’s energy minister to advance the prospect of building up to 9.6 GWe of nuclear capacity by 2030. The minister said: “This agreement opens up the door for South Africa to access Russian technologies, funding, infrastructure, and provides proper and solid platform for future extensive collaboration." It was expected to involve some $10 billion in local supply chain provision, with localization of up to 60%. Necsa later said that the new agreement "initiates a preparatory phase for the procurement process for the new nuclear build in South Africa. Similar agreements will be signed with other vendor countries that have expressed an interest in assisting South Africa with the build program...No vendor country has been chosen yet and no technology has been decided. The agreement refers only to what Russia could provide if chosen.” Rusatom Overseas confirmed the likelihood of a Russian government loan, and said that the build-own-operate (BOO) model was preferable. OKB Gidropress and NIAEP-ASE subsequently presented the VVER-TOI design as appropriate, each unit 1255 MWe gross, 1115 MWe net. The reported cost was $6 billion for the first two units.

In October 2014 a nuclear cooperation agreement with France was signed. The energy minister said, "This paves the way for establishing a nuclear procurement process." Areva welcomed the agreement, and said that it was ready to support the development of new South African nuclear projects, “notably through its Generation III+ EPR reactor technology."

In November 2014 a similar inter-governmental cooperation agreement was signed with China. The energy ministry said that the agreement "initiates the preparatory phase for a possible utilization of Chinese nuclear technology in South Africa." Three further agreements in December were between Necsa and China National Nuclear Corp (CNNC) to establish a cooperative partnership supporting the country’s nuclear industry, between China’s State Nuclear Power Technology Corp (SNPTC), the Industrial & Commercial Bank of China and South Africa's Standard Bank Group with a view to financing new nuclear plants, and between Necsa and SNPTC for training South African nuclear professional staff. In February 2015 Necsa signed a further skills development and training agreement with SNPTC and China General Nuclear Power Corp (CGN), funded up to 95% by China. CGN has had an office in Johannesburg since 2010.

Earlier in March 2014 it was reported that China’s main nuclear power companies were lining up to bid for a $93 billion contract to build six reactors by 2030. China’s Ministry of Commerce reported that negotiations towards a nuclear cooperation agreement were proceeding. The energy minister said that this could involve the joint marketing and supply of nuclear energy products along with infrastructure funding to promote nuclear power developments across the region. Chinese industry officials in December 2015 expressed confidence in securing the $80 billion order for CAP1400 units, though the first of these in China was not yet under construction at the time.

The President’s annual state-of-the-nation address in February 2015 reaffirmed the IRP 2010 9.6 GWe target with the first unit to be on line in 2023, and bids to be sought from the USA, China, France, Russia and South Korea. In May, the energy minister said that the procurement process for the new nuclear power plant would begin by September, and that a strategic partner would be selected by March 2016. Early in June Eskom ceded control of the new build programme to the Department of Energy.

Following cabinet approval in December 2015, the Department of Energy issued its request for proposals (RFP) for 9600 MWe of nuclear power capacity. Five reactor vendors were invited to make proposals: Rosatom, SNPTC, KEPCO, EDF/Areva and Westinghouse. Proposals were to specify reactor design, the degree of localization, financing, and price. Funding was to be decided following responses to this, and would be in line with IRP 2010. Necsa stressed in September 2016 that the field was wide open and that an initial contract might be for up to three PWR units, about one-third of the total, with an operating reference plant in the country of origin. It did not want a BOO arrangement or a turnkey contract, but favoured a build-own-transfer model such as in the UAE. Eskom said that there was a high level of interest in response to the December 2015 request. Formal responses were due by the end of April 2017, but in December 2016 the Treasury withdrew authorization for the RFP, and toned it down to a non-binding request for information (RFI) instead, handled by Eskom.

Then, on procedural grounds, in April 2017 the Western Cape high court set aside the intergovernmental nuclear cooperation agreements with Russia, USA and South Korea, along with approvals by the National Energy Regulator of South Africa (NERSA) of two ministerial determinations concerning the procurement of 9600 MWe of nuclear capacity. The ministerial determination signed in November 2013 and gazetted in December 2015 for a 9.6 GW nuclear new build program in South Africa was declared invalid. The ministerial determination of December 2016 appointing Eskom as the procuring agent for the nuclear new build was set aside, as was Eskom’s RFI of December 2016.

While raising issues concerning the role of government to set policy, the powers of the energy minister, and the separation of powers between the executive and judiciary, the Minister for Energy acknowledged that the government needed to start its processes afresh in conjunction with NERSA, justifying the need for the nuclear program. The CEO of Eskom was replaced, and much of the board resigned. Coincidentally, the country moved into recession, further compromising Eskom’s financial health.

The updated draft IRP published in November 2016 revised downwards the nuclear build target in its base case to 6.8 GWe coming online 2037 to 2041, and 20.4 GWe by 2050 when nuclear was to contribute 30% of electricity from 14% of capacity, compared with coal 31% from 18%. In 2050, 37.4 GWe of wind was to contribute 18% of supply, and 17.6 GWe of solar PV 6.5%. The report notes that the final updated IRP was to differ from the base case due to the impact of a number of scenarios then under consideration. For example, under the carbon budget scenario, new nuclear was likely to come online around 2026. Eskom was to continue with its request for proposals at the 9.6 GWe level, and anticipated levelized generation cost of R 1000/MWh. In April 2017, the new finance minister said that the government would “implement the [nuclear] program at the scale and pace the country can afford” on the basis of the IRP.

Due to acute water shortages in the region, Eskom announced in May 2017 that it would install a small desalination plant at Koeberg. It will produce water solely for the plant initially. Also, Eskom agreed to support the Cape Town authorities if they choose to progress plans to install a small-scale desalination unit for municipal use at the Koeberg site. It would produce 2500 to 5000 m3/d, as a demonstration plant for a larger project.

In August 2018 the South African government announced that it had abandoned plans to build up to 9600 MWe of new nuclear capacity by 2030. The draft Integrated Resources Plan (IRP) 2018 was an update of that issued in 2010, and despite endorsing the role of nuclear power did not include any new nuclear capacity by 2030. However, IRP 2019, released in October 2019, called for the country to construct two small modular nuclear reactors (SMRs) by 2030. The document also called for the completion of a 20-year operating lifetime extension at the Koeberg plant to ensure continued energy security beyond 2024, ensuring security of supply.

In May 2020, South Africa's Department of Mineral Resources and Energy stated that it was to begin working on a roadmap for the procurement of 2500 MWe of new nuclear capacity. It was considering all options, including SMRs. In August 2021 NERSA approved the plan. In December 2023 it was announced that South Africa would launch a bidding process in 2024 for 2500 MWe of new nuclear capacity. The two most likely sites to host the new capacity are Duynefontein, near Koeberg, and Thyspunt in Eastern Cape. A licence application was submitted for the site at Thyspunt in July 2021.

In January 2024 the government published plans based on the 2019 IRP to procure 2.5 GWe of new nuclear capacity. However in August 2024 the government paused the procurement process to allow for further public consultation.

In October 2025 the government approved IRP 2025. It calls for the addition of more than 105 GW of new generation capacity by 2039, including expansion of solar PV, wind and nuclear. The plan outlines the introduction of 6000 MWe of gas-powered generation by 2030 which it says is critical for energy security and stability, as well as a vision for a clean coal technology demonstration plant by 2030.

IRP 2025 calls for 5200 MWe of new nuclear capacity by 2039, with the first 1200 MWe delivered by 2036. The plan outlines the possibility of a further 4800 MWe.

In March 2026 Necsa invited expressions of interest to "identify capable technology partners… to advance a fit-for-purpose SMR technology for future deployment.”

Sites

The environmental impact assessment (EIA) process initiated earlier in 2006 confirmed the selection of three possible sites for the next nuclear power units: Thyspunt, Bantamsklip, and Duynefontein, the last of which is very near the existing Koeberg nuclear plant. All are in the Cape region and were subject to further assessment. A draft environmental impact report (EIR) was published in March 2010 recommending the Thyspunt site in Eastern Cape province near Oyster Bay, Jeffrey’s Bay and a few kilometres west of Cape St Francis. Bantamsklip is east of Cape Town near Gansbai. A final EIR was to be submitted to the Department of Environmental Affairs early in 2011. In March 2016 Eskom submitted site licence applications to NNR for both Thyspunt and Duynefontein to construct and operate "multiple nuclear installations (power reactors) and associated auxiliary nuclear installations. In December 2016 the SA Council for Geoscience confirmed the geological and geotechnical suitability of Thyspunt. In October 2017 the Department of Environmental Affairs authorized 4000 MWe nuclear capacity to be built at Duynefontein. The decision was subject to challenges from various environmental organizations, but was upheld in August 2025.

In April 2026 Eskom published a draft environmental scoping report for a further nuclear power station of up to 5200 MWe at either Thyspunt or Bantamsklip, with Thyspunt recommended as the preferred site.

Reactors proposed in South Africa

| Site | Technology | MWe gross |

Planned commercial operation |

|---|---|---|---|

| Duynefontein | ? | 4000 |

Fuel cycle

Eskom procures conversion, enrichment and fuel fabrication services on world markets. Nearly half of its enrichment is from Tenex, in Russia. However, historically South Africa has sought self-sufficiency in its fuel cycle.

A 1200 tU/yr conversion plant was established and ran in the 1980s-90s.

Enrichment was undertaken at Valindaba (also referred to as Pelindaba East) adjacent to the Pelindaba site by the unique Helikon aerodynamic vortex tube process developed in South Africa, based on a German design. Construction of the Y-Plant pilot uranium enrichment plant commenced in 1971 and was completed in 1975 by UCOR. At this time, the USA stopped exporting highly enriched uranium (HEU) fuel for the Safari-1 reactor in protest against the construction of Y-Plant and South Africa's nuclear weapons programme. Due to technical problems, Y-Plant only started producing 45%-enriched uranium in 1979 and in 1981 the first fuel assemblies for Safari-1 from Valindaba were fabricated. The Y-Plant produced about 990 kg of HEU with average enrichment of 68% until operations ceased in 1990, 336 kg of average 45% enrichment being assigned to Safari-1 for fuel or irradiation targets. The Y-Plant has been dismantled under International Atomic Energy Agency (IAEA) supervision. Much of the high-enriched uranium is stored.

On the neighbouring Pelindaba site, construction on a semi-commercial enrichment plant commenced in the late 1970s. This Z-Plant began commissioning in 1984, with full production in 1988. It had a capacity of 300,000 SWU/yr and supplied 3.25%-enriched uranium for the Koeberg plant. (Originally fuel for Koeberg was imported, but at the height of sanctionsc the AEC was asked to set up and operate conversion, enrichment and fuel manufacturing services.) Z-Plant was uneconomic and closed in 1995. It has been fully demolished.

Both centrifuge and molecular laser isotope processes were also being explored. Construction of the prototype module for the Molecular Laser Isotope Separation (MLIS) project was carried out in the Y-Plant building. The MLIS programme started in 1983 and was joined by Cogema of France in a 50:50 funding arrangement in 1995. In 1997 the programme was cancelled due to technological difficulties and AEC budget cuts.

Some fuel fabrication facilities operated from 1962. The BEVA fuel fabrication plant with 100 t/yr capacity operated in 1980-90s and supplied 330 PWR fuel assemblies for the Koeberg reactors.

A pebble fuel plant at Pelindaba was planned. Meanwhile, in December 2008, PBMR’s pilot fuel plant manufactured 9.6% enriched fuel particles, which were shipped to the USA for testing at the Idaho National Laboratory. In August 2009, PBMR (Pty) shipped 16 graphite spheres (containing 9.6%-enriched fuel particles) to Russia for irradiation tests to demonstrate the fuel’s integrity under reactor conditions. The irradiation tests, conducted by the Institute of Nuclear Materials in Zarechny near Ekaterinburg, were the final step in the development of the fuel for the PBMR demonstration unit.

A 2007 draft nuclear energy policy outlined an ambitious programme to develop all aspects of the nuclear fuel cycle, including a return to conversion, enrichment, fuel fabrication and also reprocessing of used fuel as strategic priorities related to energy security. A new 5.0 to 10.0 million SWU/yr centrifuge enrichment plant built in partnership with Areva (now Orano), Urenco or Tenex was envisaged, the larger version allowing scope for exports. With 9600 MW of new capacity then assumed, a significant level of local content in fuel cycle services was anticipated.

Initial feasibility studies on the re-establishment of nuclear fuel cycle programmes were completed in 2011. South Africa’s proposed new power plants were expected to need about 465 tonnes of enriched uranium annually by 2030. Necsa proposed to establish fuel fabrication capacity for PWRs "to ensure eventual security of fuel supply for South Africa." In March 2013 Westinghouse signed a cooperation agreement with Necsa on development of local facilities for fuel assembly components.

In 2012 the vision was for 1800 tU/yr conversion plant, 1.3 million SWU/yr enrichment plant and 200 tU/yr fuel fabrication plant, all established at one fuel cycle site from 2016. The conversion capacity was to possibly involve re-commissioning the old plant, or an international joint venture to commission in 2026. Enrichment would be by centrifuge, possibly with an international partner, to commission in 2026-27. Fuel fabrication was to be in partnership with the new nuclear plant vendor.

Uranium mining

Uranium production in South Africa has generally been a by-product of gold or copper mining.

In 1951, a company was formed to exploit the uranium-rich slurries from gold mining and in 1967 this function was taken over by Nuclear Fuels Corporation of South Africa (Nufcor), which in 1998 became a subsidiary of AngloGold Ltd (later AngloGold Ashanti), and in 2018 was acquired by Harmony Gold Mining. Over nearly 30 years to 1980 it had produced some 100,000 tonnes of uranium oxide from varied feed, at a peak rate of almost 6000 t/yr in 1960. The plant is 60 km west of Johannesburg, adjacent to West Rand mines, in Gauteng province. In May 2009 AngloGold announced plans to construct a new uranium recovery plant at its Kopanang mine to lift production to 900 t/yr from 2012, but did not proceed.

There are about 400 tailings dams and dumps arising from gold mining in the Witwatersrand area of Gauteng province, and much of the available uranium today is in these. There are further tailings near Klerksdorp, close to the Vaal River. There is some radionuclide and heavy metal pollution arising from some of these and acid mine drainage. Many of the tailings dams and dumps are being re-treated to recover gold and sometimes uranium.

In October 2017 Anglo Gold Ashanti announced that it was selling assets in the Vaal River region to Harmony Gold Mining for $300 million. The assets are: Moab Khotsong mine and related infrastructure; its entire interest in Nuclear Fuels Corp of South Africa (Nufcor); and its entire interest in Margaret Water Company. The sale was completed in 2018, and in 2020 AngloGold Ashanti sold its remaining South African assets – the Mponeng mine and Mine Waste Solutions (MWS) surface operations – to Harmony.

At the end of March 2020, the government imposed a 21-day lockdown in response to the coronavirus pandemic. As part of the lockdown, all mining operations (apart from coal mines supplying Eskom) were initially suspended. The lockdown regulations were amended in mid-April to allow mining to resume at up to 50% of normal capacity.

Uranium production (tonnes U)

| 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | |

| Ezulwini-Cooke | 34 | 0 | 0 | 69 | 47 | 67 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Vaal River | 548 | 465 | 531 | 504 | 346 | 423 | 308 | 346 | 346 | 250 | 192 | 200 | 200 | 200 |

| Total | 582 | 465 | 531 | 573 | 393 | 490 | 308 | 346 | 346 | 250 | 192 | 200 | 200 | 200 |

Much of the productive and prospective ground for uranium as gold by-product is in the Witwatersrand Basin, an area about 330 km x 150 km south and southwest of Johannesburg. Klerksdorp, Welkom, Carltonville, Parys and Evander are towns also on its fringes, associated with gold mines.

Cooke, with Ezulwini – Sibanye

First Uranium Corp of Canada built a US$ 55 million uranium processing plant at Ezulwini gold-uranium mine in the West Rand, 40 km southwest of Johannesburg, which has 3200 tU in measured and indicated resources and 85,000 tU inferred resources. The main part of the plant, part of a $280 million recommissioning project, was completed and the first uranium produced in May 2009. Calcining is off-site, by Nufcor. A seven-year ramp-up of underground production from the Middle Elsburg reef was planned, but the uranium plant was placed on care and maintenance in February 2012. FY 2012 production (to end March) was 34 tU. The mine earlier produced over 6000 tU from 1961 to 2001. In August 2012 Gold One bought the mine and plant for $70 million, and it became Cooke 4.

Gold One planned to recommission the Ezulwini plant by March 2013, to treat both gold and uranium separately. The mine would form part of the company’s Cooke underground operations, but in August 2013 Sibanye Gold Ltd (spun off from Goldfields in February 2013) bought the whole Cooke operation, with all of the underground and surface plant, and including the dumps. Sibanye issued Gold One with about 150 million shares, some 17% of the company.

Nearby, Rand Uranium was spun off from Harmony Gold Mining Co and in joint venture with Pamodzi Resource Fund was reopening part of the Randfontein mine (also in Gauteng, 40 km west of Johannesburg). The mine, at the western end of the main Witwatersrand gold orebody, produced uranium in the 1980s, though its Cooke section had only been mined for gold. Rand identified JORC-compliant resources of some 41,000 tU both in tailings and underground. This included probable reserves of 15,200 tU in the Cooke tailings, which comprised the chief asset of the new company. Production at 1000 tU/yr was envisaged, but Randfontein Surface Operations (RSO) became part of the Cooke underground operations of Sibanye by about 2013.

The shallow Cooke 1, 2&3 mines, Cooke 4 including Ezulwini, and Randfontein Surface Operations comprise the Cooke operation of Sibanye, which describes it as a short- to medium-term asset, with life of mine estimated to extend to 2023. Cooke A1 proved & probable reserves were 1180 tU at 0.028%U in total A1 resources of 9420 tU at 0.045%U, with 16,950 tU as B1 inferred resources at the end of 2015. The Ezulwini plant enables recovery of uranium as by-product of about 4 tonnes of gold production annually. Cooke 4 is a 1634 m deep mine adjacent to Ezulwini plant, and a separate part of the operation.

Underground material from Cooke 1, 2&3 is processed at the Doornkop plant, operated by Harmony Gold Mining Company Ltd, on a toll treatment basis for recovery of gold. Run-of-mine ore from Cooke 4 is treated at the Ezulwini gold-uranium plant near Cooke 4 Shaft. Ore from the uranium section at Cooke 3 is hoisted separately and trucked to the Ezulwini gold-uranium plant for treatment.

In May 2014 Sibanye sent its first consignment, of 10 tonnes ammonium diuranate, from Ezulwini/Cooke to Nufcor for calcining to U3O8. In 2014, 69 tonnes of by-product uranium from Cooke was stockpiled. Production in 2015 was 47 tU, also stockpiled. Production in 2016 was 67 tU. The company earlier expected to ramp up to 230 tU/yr by-product by 2016.

In July 2016 Sibanye Gold said that over 17 months the Cooke 4 operation had failed to meet production and cost targets, and losses had accumulated. It was declared uneconomic in August 2016.

West Rand Tailings Retreatment Project (Driefontein and Kloof)

The measured and indicated resources/probable reserves at Sibanye’s West Rand Tailings Retreatment Project (Driefontein, Kloof and Cooke historical tailings) in Gauteng province were 38,190 tU at 0.0054%U at the end of 2015. A feasibility study was underway in 2016, but in 2018 the project was sold to DRDGOLD, which processes the tailings for gold only.

(Driefontein has six operating shaft systems and three metallurgical plants, and operates at depths of 700 m to 3400 m below surface. Kloof is an intermediate to ultra-deep level mine with operating depths of between 1300 m and 3500 m below surface. Both are major gold producers.)

Beatrix

Sibanye Gold has its main operation at Beatrix, 20 km south of Welkom, in the Free State province 240 km southwest of Johannesburg. The company describes it as a low-cost and high-productivity operation with life of mine to about 2029. Sibanye announced uranium resources (SAMREC code) at December 2013 for Beatrix West Section – previously Oryx – on the Beisa reef of 9900 tU at 0.079%U. In February 2016 the company announced a maiden A1 probable reserve for Beisa of 4490 tU at 0.06%U, in A1 measured and indicated resources of 10,390 tU at 0.09%U. Beisa North has inferred resources of 13,630 tU at 0.09%U. In early 2016 the company completed a feasibility study on the project. The Beisa mine had been closed in 1984 by the predecessor of Goldfields. The company said it might construct a uranium plant at Beatrix or ship all the uranium north to be processed at the Cooke 4 Ezulwini plant in West Rand. In December 2024 Sibanye-Stillwater agreed to sell the Beatrix 4 shaft, including the Beisa uranium project, to Neo Energy Metals for R500 million.

Buffelsfontein, Vaal River – Anglo Gold Ashanti surface operations

First Uranium had been building a larger $260 million uranium processing plant at the Buffelsfontein gold mine in the North West province, 160 km from Johannesburg and within the Klerksdorp gold field of the Witwatersrand basin. It is about 10 km east of Klerksdorp, and has some 21,000 tU as proven and probable reserves in old mine tailings, some near Stilfontein – its Mine Waste Solutions (MWS) project. The MWS tailings dams cover an area about 14 km across. Uranium production was expected to be 600 tU/yr over 16 years at full capacity, ramping up to 350 tU/yr from late 2010. The provincial government in July 2009 approved construction of a large new tailings storage facility for MWS, and a new plant was due to be commissioned in 2014. AngloGold Ashanti acquired the operation for $335 million in mid-2012.

Anglo Gold Ashanti produced uranium as by-product from its Surface Operations division which extracted gold from marginal ore dumps and tailings storage facilities on surface at various Vaal River and West Wits operations. Surface Operations included MWS, which operated independently. The company quoted by-product resources (mostly indicated) of 130,560 tonnes U3O8 including by-product reserves (mostly probable) of 53,700 t U3O8 at the end of 2015. Some 60% of the resources were in MWS or other surface tailings.

Uranium is produced at Vaal River by processing the reef material from Moab Khotsong, Great Noligwa and Kopanang, all next to the Buffelsfontein mine. The reef ore is milled at the Noligwa Gold Plant and processed at the South Uranium Plant for uranium oxide extraction by the reverse leach process. Ammonium diuranate (‘yellowcake’) is the final product of the South Uranium Plant and is transported to Nufcor (located in Gauteng) where the material is calcined and the U3O8 packed for shipment to the converters.

Total production in 2013 was 532 tU, partly as by-product from the Great Noligwa mine. Later production is tabulated above. In 2017 the company said it would close or sell Kopanang. Moab Khotsong, under Harmony Gold Mining’s ownership since 2018, is now South Africa’s only significant source of uranium production.

Both Shiva and MWS operations are in the Klerksdorp area southwest of Johannesburg, and in 2008 First Uranium announced plans to build an acid plant using pyrite from MWS and 30 MWe of power generating capacity to service the two operations.

Shiva/Dominion Reefs

In 2006, Uranium Oned obtained its mining right for the Dominion Reefs project at Haartebeesfontein, 20 km east of Klerksdorp in the North West province,160 km southwest of Johannesburg. This had been the northern part of the adjacent Buffelsfontein Gold Mine operation. Production commenced early in 2007 and was planned to increase to 1730 t/yr U3O8 by 2011. Production cost was earlier expected to be US$ 14.50/lb U3O8 from the conglomerate reefs to 500 metres depth, but evidently increased well beyond this. The first sales contract for 680 tonnes was announced in November 2006. Production in 2007 was 78 tonnes and that for 2008 was 86 tonnes U3O8, reflecting slower and more difficult underground development than anticipated. A small amount of uranium was purchased from Australia in 2008 to meet sales commitments.

Dominion, including the Rietkuil section, had indicated resources of 51,000 tonnes U3O8 at 0.063% and inferred resources of 62,800 tonnes U3O8 at 0.036%. Within these, reserves however are only 14,240 tonnes at 0.077% and with US$ 46.50/lb production cost. The mine was closed in October 2008 due to a labour dispute coupled with power shortages and increased project costs in the context of lower uranium spot prices. The mine was then put on care and maintenance.

Uranium One sold it in April 2010 for $37 million to Shiva Uranium, a 74% subsidiary of Oakbay Resources & Energy Ltd, which is 85% Indian-owned. Shiva resumed uranium production early in 2011, but since then only gold has been produced while uranium workings are developed with a view to substantial production. The onsite uranium plant is the only one in South Africa using pressure leaching, which achieves uranium recovery of up to 92%, significantly more than other leaching methods. In June 2019 the mine was put up for auction, but no sale resulted.

Karoo

Australian-based Peninsula Energy has reported a JORC-compliant resource of 21,930 tU at its Karoo project straddling the East and West Cape provinces. This includes indicated resource of 8440 tU grading 0.089%U in sandstone. Drilling converted historical resource information from the 1970s to JORC-compliant. Some of the resources in the Ryst Kuil channel have molybdenum byproduct. Peninsula held a 74% interest in the project, the remaining 26% is held by black economic development partners. In April 2018 Peninsula announced that it was withdrawing from Karoo in order to focus attention on its Lance project in the USA. Surface rehabilitation was subsequently completed and Peninsula applied for regulatory closure of the project.

Uranium and molybdenum mineralization is hosted in fluvial channel sandstone deposits chiefly in the western and central parts of the Main Karoo basin. The occurrences are epigenetic, tabular and sandstone-hosted, and the thickest sandstone bodies tend to contain the highest proportion of mineralization. The company’s further exploration target was up to 110,000 tU.

The Ryst Kuil part of the Karoo project was held by Uramin Inc, which was then taken over by Areva (now Orano) to become Areva Resources Southern Africa. The deposit had been discovered by Esso in the 1970s. Some 16,000 tU resources were estimated on historic basis at 0.1% grade. Areva suspended the project at the end of 2011, and in April 2014 it was acquired by Peninsula Energy to form part of the Karoo project. The Ryst Kuil channel was the focus of exploration until Peninsula’s withdrawal.

Namakwa/Henkries

The Namakwa Henkries uranium project in the Northern Cape province is being explored by Namakwa Uranium, which is now owned 74% by Aarvark Uranium Ltd and 26% by the company's black economic development partner, Gilstra Exploration. Anglo American did a feasibility study on the project in 1979. Xtract Resources investigated the prospect in 2014, but did not proceed with acquisition.

Waste management & decommissioning

The 2008 National Radioactive Waste Disposal Institute Act provides for the establishment of the National Radioactive Waste Disposal Institute (NRWDI) to be responsible for radioactive waste disposal in South Africa. Establishment of this was announced in March 2014.

Necsa had been operating the national repository for low- and intermediate-level waste at Vaalputs in the Northern Cape province. This was commissioned in 1986 for waste from Koeberg and is financed by fees paid by Eskom. From about 2008 this Vaalputs facility became the National Radioactive Waste Disposal Facility, and continued to be managed by Necsa. In July 2025 a licence was granted for NRWDI to manage and operate the facility. Some low- and intermediate-level waste from hospitals, industry and Necsa itself is disposed of at Necsa's Pelindaba site.

Used fuel is stored at Koeberg. In May 2015 Holtec won a contract from Eskom to supply HI-STAR 100 dual-purpose metal casks for transport and storage of used fuel by September 2018. In December 2024 the National Nuclear Regulator opened public consultation on an Eskom application to expand cask storage capacity at the plant. The National Radioactive Waste Disposal Institute is planning a centralized interim storage facility at Vaalputs to accommodate used fuel from Koeberg.

Earlier, in August 2008, the nuclear safety director of the Department of Minerals and Energy announced that Eskom would seek commercial arrangements to reprocess its used fuel overseas and utilize the resulting mixed oxide (MOX) fuel. This has not yet proceeded.

Research & development

Necsa was established from the Atomic Energy Corporation (AEC) as a public company under the 1999 Nuclear Energy Act, and is wholly-owned by the state. Its main functions are to undertake and promote research and development in the field of nuclear energy and radiation sciences and technology, and to process source material, special nuclear material and restricted material.

Necsa operates the 20 MWt Safari-1 reactor at its Pelindaba nuclear research centre. Safari-1 is the main supplier of medical radioisotopes in Africa and can supply up to 25% of the world's molybdenum-99 needs. By 2009 the reactor was converted from using HEU to low enriched uranium (LEU) fuel3, and conversion of the targets used for radioisotope production from HEU to LEU was achieved in 2010. Following this, Necsa and its subsidiary NTP Radioisotopes (Pty) Ltd in October 2010 were awarded a $25 million contract by the US Department of Energy's (DoE's) National Nuclear Security Administration (NNSA) to supply Mo-99. Mo-99 from Safari is supplied to US-based Lantheus Medical Imaging, which makes Tc-99 generators. The commercial-scale production of the medical isotope from low-enriched uranium is in collaboration with the Australian Nuclear Science and Technology Organization (ANSTO), whose 20 MWt Opal reactor also uses LEU fuel and targets for Mo-99 production.

With the end of operating life of Safari in sight, proposals have been for the Dedicated Isotope Production Reactor (DIPR) and, with more probability, a new research reactor which includes isotope production among other roles. In September 2021 the government approved construction of the Multipurpose Reactor to replace Safari. In February 2025 the government approved the detailed design phase of the project and allocated R1.2 billion ($66 million), with the reactor targeted to be in operation in about 2032-2033. Safari-1 is currently licensed to operate to 2030, and Necsa is seeking a licence extension so that the two reactors can run in parallel.

Klydon Corporation, which emerged from the AEC, has been developing its Aerodynamic Separation Process (ASP) employing so-called stationary-wall centrifuges with UF6 injected tangentially. It is based on Helikon but, pending regulatory authorization from Necsa, has not yet been tested on UF6 – only light isotopes such as silicone which it is evidently most suited to. Klydon Element 92 Division is focused on uranium prospects, while its Stable Isotopes Division is concerned with silicon-28, zirconium-90 and medical isotopes.

Pebble Bed Modular Reactor (PBMR)

Over 1993 to 2010, Eskom (in collaboration with others since 1999f) was developing the Pebble Bed Modular Reactor (PBMR). It is a high-temperature gas-cooled reactor (HTR) design, for both electricity generation (through a steam turbine or direct cycle) and process heat applications, with helium outlet temperatures up to 940°C. From 1999 to 2009, the South African government, Eskom, Westinghouse, and the Industrial Development Corporation of South Africa invested R9.244 billion (about $1.3 billion) in the projectg. The original concept was for a 400 MWt direct (Brayton) cycle unit, but later a 200 MWt (80 MWe) steam cycle version was proposed.

In September 2010, the Minister of Public Enterprises announced that the government would stop investing in the PBMR4. The minister gave the following reasons for this decision:

- No customer for the PBMR had been secured.

- In addition to the R9.244 billion ($1.3 billion) already invested in the project over the previous decade, a further R30 billion ($4.2 billion) or more was needed.

- The project has consistently missed deadlines.

- The opportunity to participate in the USA’s Next Generation Nuclear Plant (NGNP) programme had been lost (see below).

- Any new nuclear build programme in South Africa would use Generation II or III technology. (The PBMR is considered a Generation IV technology.)

- Government spending had to be reprioritized in the light of the economic downturn.

The project had received a certain amount of interest, but not enough to secure the financing it required. The domestic need in South Africa is for larger units.

Eskom is managing the PBMR assets. The main PBMR test facilities (fuel development laboratory and helium test facility) are in care and maintenance. The government is concerned to protect the intellectual property involved.

An August 2013 application for federal US funds from National Project Management Corporation (NPMC) in the USA was for an HTR of 165 MWe, apparently the earlier direct-cycle version of the PBMR, emphasising its ‘deep burn’ attributes in destroying actinides and achieving high burn-up at high temperatures.

In mid-2013 a nuclear cooperation agreement was signed with the EU, to support research, with PBMR and medical isotopes mentioned. This was to be implemented by Euratom.

In 2016 Eskom revived consideration of a reactor based on the PBMR, with a view to developing a design that is simpler and more efficient than the original, and also looking at applications for process heat that were not fully explored by the original R&D programme. Also a small-scale nuclear reactor could complement the intermittency of renewable sources.

A new concept is for an advanced high-temperature reactor of 150 MWe to be deployed in the 2030s, with a 50 MWe pilot plant built in the mid-2020s. It will be a combined-cycle plant with gas flow now from bottom to top, and the temperature will be much higher. The pressure vessel would be concrete, fuel would be pebbles. Helium would exit the reactor to a gas turbine at 1200°C, and the exhaust gas from this at 600°C would drive a steam cycle, using a molten salt circuit, with overall 60% thermal efficiency. The gas turbine would produce 40% of the power, the steam cycle 60%.

In November 2025 the Cabinet approved lifting the PBMR project from care and maintenance and transferring PBMR (SOC) Ltd from Eskom to Necsa.

A private company built on PBMR experience, Steenkampskraal Thorium Limited (STL Nuclear), is developing the HTMR-100, a 35 MWe (100 MWt) pebble bed HTR for electricity or process heat. The conceptual design (formerly known as the Th-100) commenced in 2012 and is aimed at the African market. It is derived from the Jülich and PMBR designs but operates at a lower temperature than the PBMR. For electricity, single units can utilize load-following capability, or four can comprise a 140 MWe power plant. There is a range of fuel options but the focus is on a thorium-based fuel cycle, with slow single pass of TRISO fuel pebbles giving higher burn-up. It has a graphite moderator and helium coolant at 750°C driving a steam cycle. An HTMR-30 is also being designed to generate 10 MWe, and a smaller microreactor of 10 MWt is being developed.

Regulation, safety and non-proliferation

In 1948, the Atomic Energy Act created the Atomic Energy Board, which later became the Atomic Energy Corporation (AEC). In 1963, the Nuclear Installations Act provided for licensing and in 1982 the Nuclear Energy Act made the AEC responsible for all nuclear matters including enrichment. An amendment to it created the autonomous Council for Nuclear Safety, responsible for licensing.

The Nuclear Energy Act of 1999 gives responsibility to the Minister of Minerals & Energy for nuclear power generation, management of radioactive wastes and the country's international commitments. The South African Nuclear Energy Corporation (Necsa) is a state corporation established from the AEC under the Act, and is responsible for most nuclear energy matters including wastes and safeguards, but not power generation.

The National Nuclear Regulator Act of 1999 sets up the National Nuclear Regulator (NNR) – previously the Council for Nuclear Safety – covering the full fuel cycle from mining to waste disposal, and in particular the siting, design, construction, operation and decommissioning of nuclear installations. The NNR is being strengthened in preparation for an expanded role with new nuclear power plants. In November 2015 NNR established a relationship with China’s National Nuclear Safety Administration (NNSA) to collaborate on several fronts and benchmark its regulatory practices.

Following a 2024 restructuring in which the Department of Mineral Resources and Energy was split, the Department of Electricity and Energy has overall responsibility for nuclear energy and administers the above acts. Eskom, previously under the now-dissolved Department of Public Enterprises, also falls under the Department of Electricity and Energy.

The Department of Minerals and Energy (DME) has overall responsibility for nuclear energy and administers the above Acts. However, Eskom is under the Department of Public Enterprises.

The Department of Forestry, Fisheries and the Environment is responsible for environmental assessment of projects, and has a cooperative agreement with the National Nuclear Regulator for nuclear projects.

An IAEA Integrated Nuclear Infrastructure Review (INIR) mission was undertaken early in 2013 to evaluate the status of the country’s nuclear infrastructure development. It was the first such mission to a country with established nuclear power.

Non-proliferation

Having been a foundation member of the IAEA in 1957, South Africa is the only country to develop nuclear weapons and voluntarily give them up. It embarked on a nuclear weapons programme around 1970 and had a nuclear device ready by the end of the decade. The weapons programme was terminated by President F. W. de Klerk in 1990 and, in 1991, the country signed the Nuclear Non-Proliferation Treaty (NPT). In 1993, de Klerk announced that six nuclear weapons and a seventh uncompleted one had been dismantled. In 1995, the International Atomic Energy Agency (IAEA) was able to declare that it was satisfied all materials were accounted for and the weapons programme had been terminated and dismantled.

In 1996, South Africa signed the African Nuclear Weapon Free Zone Treaty – also called the Pelindaba Treaty. In 2002, the country signed the Additional Protocol in relation to its safeguards agreements with the IAEA. South Africa is member of the Nuclear Suppliers' Group, and the country’s dual-use capabilities are regulated by the South African Council for the Non-Proliferation of Weapons of Mass Destruction (NPC).

Notes & references

Notes

a. In 1944, the USA and UK requested forecasts from South Africa on its potential to supply mineable uranium. This led to the formation of the Uranium Committee in 1945, and, in 1948, the Atomic Energy Board (AEB) was formally established to oversee uranium production and trade. In 1959, research, development and utilization of nuclear technology was added to AEB's remit. In 1970, the Uranium Enrichment Corporation (UCOR) was established, initiating an extensive fuel cycle programme. In 1982, the AEB was re-established as the Nuclear Development Corporation of South Africa (NUCOR) under a new controlling body – the Atomic Energy Corporation of South Africa (AEC). In 1985, UCOR was incorporated into the AEC. The South African Nuclear Energy Corporation (NECSA) was formed out of the AEC in 1999. [Back]

b. The Safari-1 (South African Fundamental Atomic Research Installation) reactor initially operated at 6.75 MW and was upgraded to 20 MW in 1968. The pool-type reactor is an Oak Ridge National Laboratory (ORNL) design fuelled by highly enriched uranium (HEU). A program to convert to low enriched uranium (LEU) fuel commenced in 2006. [Back]

c. South Africa's policy of apartheid – which ended with the 27 April 1994 general election – attracted extensive international sanctions. However, it was not until the late 1970s/early 1980s that international pressure intensified, culminating in 1985-1991 with trade sanctions by the USA, British Commonwealth and Europe, as well as disinvestment campaigns in many countries. [Back]

d. See the Uranium One website (www.uranium1.com) [Back]

e. Extrapolating from test results, ASP is expected to have an enrichment factor in each unit of 1.10 (cf 1.03 in Helikon) with about 1000 kWh/SWU. Development of it is aiming for 1.15 enrichment factor and less than 500 kWh/SWU (compared with about 10,000 kWh/SWU in the Z-plant). However, to achieve gas speeds sufficient for enrichment, heavy elements such as uranium need to be greatly diluted with hydrogen, and the process appears uneconomic for uranium. [Back]

f. Eskom held all the shares in the PBMR company, PBMR (Pty) Ltd., but several investment partners provided financing for the feasibility stage of the project. In June 2000, the UK's British Nuclear Fuels Limited (BNFL) took a 22.5% stake in the venture. Soon after, US utility PECO (later Exelon, following the merger with Commonwealth Edison) took a 12.5% stake. The South African government-owned Industrial Development Corporation (IDC) took 25%, leaving Eskom with 40%, of which 10% was reserved (but never taken up) for an Economic Empowerment Entity. Exelon withdrew from the project in April 2002. Also, around the same time, BNFL reduced its stake to 15%, and IDC reduced its to 13%. In 2006, BNFL's 15% stake was transferred to its Westinghouse subsidiary, which was later sold to Toshiba.

Under an investors' agreement made in 2005, BNFL/Westinghouse had a 15% stake, IDC 14%, the South African government 30%, leaving Eskom with 41%. These shares were expected to move to 4% Westinghouse, 15% IDC, 30% South African government and 5% Eskom by 2012, with 46% being held by another investor. However, in August 2006, this agreement lapsed and a new agreement could not be reached. (Had a new investors' agreement been reached, Westinghouse would have had rights to 5% of the company, the South African Industrial Development Corporation to 5%, and 81% for the government, leaving Eskom with 9%.)

Although PBMR (Pty) Ltd continued to list its investors as the South African government, IDC, Westinghouse and Eskom, its funding following the completion of the feasibility stage in 2004 was principally from the South African government (through its Department of Public Enterprises). In March 2010, the government drastically cut funding for the PBMR, then in September 2010 it announced that all funding was to be cut. [Back]

g. Of the R9.244 billion (about US$ 1.3 billion) invested in the PBMR project, the South African government contributed 80.3%, Eskom 8.8%, Westinghouse 4.9%, the Industrial Development Corporation of South Africa 4.9%, and Exelon 1.1%. Figures given by Barbara Hogan, Minister of Public Enterprises, to the National Assembly on 16 September 2010 (see Reference 9 below). [Back]

References

1. Southern African Power Pool Annual Report 2020 [Back]

2. Eskom shelves new nuclear project, World Nuclear News (5 December 2008) [Back]

3. Nuclear Reactor Uses Only Low Enriched Uranium (LEU) for the First Time, South African Nuclear Energy Corporation media release (29 June 2009). See also announcement from 2005: Minister of Minerals and Energy announces the phasing out of the use of High Enriched Uranium for the Pelindaba Research Reactor Nuclear Fuel, Department of Minerals and Energy statement (18 July 2005) [Back]

4. PBMR postponed, World Nuclear News (11 September 2009) [Back]

General sources

International Atomic Energy Agency, Country Nuclear Power Profiles

South African Nuclear Energy Corporation website (www.necsa.co.za)

PBMR (Pty) Ltd. website (www.pbmr.co.za)

Eskom website (www.eskom.co.za)

State Owned Enterprises page on the Department of Public Enterprises website (www.dpe.gov.za)

Department of Energy, Integrated Resource Plan (IRP) 2010, 2016, 2018

Department of Energy, Integrated Energy Plan (IEP), November 2016

Department of Energy, IRP Update Assumptions and Base Case presentation, November 2016