Financing Nuclear Energy

- Nuclear power plants are large infrastructure investments with century-long footprints.

- A nuclear power plant project is characterised by high upfront capital costs and long construction periods, low and stable operational costs, and lengthy payback periods.

- This investment profile, combined with the risks associated with construction, mean that the cost of financing is a key determinant of the cost of electricity generated.

- Typically it is the responsibility of owners or operators of nuclear power plants to secure financing for new nuclear power plants. For investors, the confidence provided by clear, long-term governmental commitment to a nuclear power programme remains critical.

- Most nuclear power plants in operation were financed in regulated energy markets, where returns on investment were generally secure. Widespread deregulation of markets has altered the risk profile related to investing in new capacity because electricity prices are less predictable.

- A significant number of models have been used in recent years to facilitate investment. Most combine a long-term power purchase contract, to reduce revenue risk, and a means of capping investor exposure, for example through loan guarantees.

The importance of competitive finance

Nuclear power provides a source of reliable, low-carbon electricity, and it is widely recognised that its role will need to grow to reduce carbon dioxide emissions in order to mitigate climate change. One of the principal barriers to the necessary expansion is the challenge associated with securing competitive financing for new nuclear plants.

A nuclear power plant as an investment is fundamentally no different to that of any large infrastructure project: it is characterised by high upfront capital costs and a long construction period, followed by a lengthy payback period – and it will be financed, typically, by a mix of debt and equity. However, there are several features specific to nuclear projects that present unique considerations for investors:

- Technical complexity – presenting (relatively) high risks during the construction phase of delays and cost overruns.

- Political and regulatory risks – long, expensive, and changeable permitting and licensing regimes.

- Liabilities – related to waste management and decommissioning.

- High fixed to variable cost ratios – a challenge in markets with uncertain electricity pricing and demand. This cost profile is a feature of all low-carbon electricity generation options, in contrast to fossil fuel generated electricity, where the fuel itself is the principal cost.

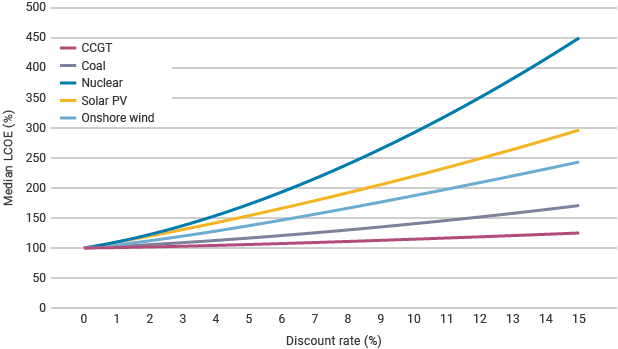

For any infrastructure project, in addition to the actual capital expended, there is a cost to pay related to the provision of that capital. Loans raised to cover the investment costs must be repaid to lenders at agreed intervals, and similarly, equity investors will demand a reasonable rate of return. Among electricity generation technologies, the cost of finance is particularly important for the overall economics of nuclear power plants due to the profile of the capital expenditure. Nuclear power plants are more complex than other large-scale power generation plants, and so are more capital-intensive and may take longer to construct. Typically a nuclear power plant will take over five years to construct whereas natural gas-fired plants are frequently built in about two years. Once in operation, the high capital costs of nuclear construction are offset by low and stable variable costs, but the need to finance the upfront construction costs presents a challenge.

The cost of capital is typically a key component of the overall capital cost of nuclear power projects. Over a long construction period, during which there are no revenue streams from the project, the interest on funds borrowed can compound into very significant amounts. In a business plan, the cost of capital is often calculated at various discount rates to discover whether capital expenditure can be recovered. If the cost of capital is high then the capital expenditure rises disproportionately and may undermine the viability of the project.

Effect of discount rate on median levelized cost of electricity (LCOE)a

The LCOE of nuclear is particularly sensitive to discount rate because of the technology's high fixed to operating cost ratio

Source: OECD Nuclear Energy Agency.

Historical perspective

The cost of capital depends on investors’ judgement of the project completion and market risks involved. For a power plant, that judgement will be a function of who the investors are, as well as many other factors, including: the regulatory and market framework in which the plant is built; the project promoter’s track record; the relative novelty of the reactor design being used; and the national energy policy and political situation.

In the 1970s and 1980s a large amount of capital was mobilised to support the grid connection of nearly 400 reactors. There were many factors that contributed to this distinct period of high growth, including the oil price shocks of the 1970s that led to acute security of supply concerns, but an important difference relates to market design. During the 1970s, most plants were built in energy markets regulated by governments, where electricity customers paid a standard price for the power. For utilities investing in large power plants, regulated markets provided a high degree of assurance that their costs would be passed onto electricity consumers. Further, during the 1970s and 1980s, most utilities were government-owned, meaning that investment could be financed directly through the public purse, or be supported by an implicit government guarantee.

In the period since, many formerly regulated markets have been restructured and deregulated in order to introduce a degree of competition. Customers gained the freedom to choose their energy supplier and power producers competed to sell their electricity into a wholesale market. In a competitive market, there is no guarantee for an investor or operator that it will find a ready market with prices high enough to provide an acceptable return on investment. Such changes to electricity market structure have important implications for the level of financial risk assumed by investors.

Deregulated markets have generally proved successful at reducing the wholesale price of electricity. However, they also introduced greater uncertainty and price volatility, and it is increasingly clear that they do not provide sufficient price signals to ensure required new capacity is built. This is particularly true for electricity generating technologies that may be competitive on a lifetime cost basis, but have a high ratio of fixed costs to variable costs – a cost structure shared by all low-carbon electricity generating options.

Funding

Regardless of market design, a project needs to be economically viable to attract finance. In other words, it needs a clear revenue stream greater than operating and capital costs. In competitive wholesale markets with volatile prices, there may not be a clear funding stream that is satisfactory to investors. Governments have sought to address these issues through a number of mechanisms and developers have looked at different project structures to reduce and better-distribute risk among parties.

Government and corporate finance

Broadly, there are two main ways in which a nuclear power project and its ownership can be structured: government (public) or corporate (private) finance.

| Structure | Description | Examples |

| Public (i.e. government) |

Government directly finances a project through a mix of equity and debt. Availability depends on government policy and market design. Not an option in many countries, for example the UK. Typically takes place in markets where governments are also involved in owning and operating energy utilities. Government involvement in a project, even if indirect (e.g. a government holds a majority stake in the utility), usually makes it much easier to raise cost-effective debt. Most operating plants were financed in this way. |

Qinshan 1 in China |

| Private (i.e. corporate) |

Finance is raised within private companies (i.e. from the balance sheet) through a mix of debt and equity. Most commonly the corporate entity is a large utility. The corporate entity arranges credit from lenders and takes on the full risk related to the project. In some circumstances, groups of investors may choose to cooperatively finance a project (see below). |

Widely used in France, Korea, Russia, the UK and USA |

Investor/cooperative financing

Private investment may be facilitated through cooperative investment models, where a group of investors raise debt and equity for a project, and share the risk related to doing so.

In Finland since the 1970s almost all large power plants have been financed by the private sector through a model known as Mankala. This model is a form of cooperative corporate finance, where the risks of large energy investments are shared among a group of companies. In the model, energy producers are owned by a number of companies that jointly bear the costs of constructing and operating a plant through the provision of equity finance. Mankala companies are limited liability companies, but do not pay dividends to shareholders. Instead, each owner, proportional to its share of equity, is allowed (and obliged) to purchase energy from the company on a cost-price basis. The energy purchased may be sold or used by the purchaser. Investors are typically wholesalers, retailers or large industrial companies.

The model has proved successful in Finland, enabling two-thirds of the country’s electricity to be produced at cost price. However this financing route depends on there being a sufficient number of energy-intensive industries willing and able to participate in a project.

In France, a financing structure was established between 2005 and 2010 where a number of industrial investors and banks formed the Exceltium consortium to negotiate an optimal electricity supply contract on behalf of its shareholders. Much like the Mankala model, the purpose for investors was to enter into a contract with EDF to help finance its new plants in return for cheaper electricity. Industrial investors are paid back over a period of 24 years. The industrial investors can choose to use the electricity themselves or sell it into the market.

Limited versus full-recourse financing

Finance for a project can be raised on a limited/non-recourse basis or on a recourse basis. If a project is financed on a recourse basis, lenders’ collateral is provided by the existing assets of the project’s promoters. In the case of limited-recourse financing (or project financing), by contrast, the capital raised is backed only by the project itself.

In the case of project finance, a separate corporate entity is set up to own the project, and shares in the new entity are bought by participants in the project. Debt may be raised to pay for part of the construction cost, but lenders' only collateral will be the shares in the project company itself. As a result, whilst the arrangement has the advantage of shielding equity holders’ other assets, it is riskier for lenders. It is normally therefore more difficult and expensive to obtain loans from lenders.

Project finance is used widely in the power sector, but mainly for renewable projects and natural gas turbines – assets that are less capital-intensive, more flexible and have shorter construction times. It has not been used in any significant way for nuclear power plants or hydropower projects.

Contracts guaranteeing future revenues (see section below) may provide some additional security to lenders, but such arrangements are of limited value in a non-recourse arrangement if the project fails or the plant is prevented from operating. Until a promoter can demonstrate a strong track record of building and operating nuclear plants with a standardised design, it is unlikely that nuclear plant projects will be financed on a limited-recourse basis.

Encouraging investment: reducing revenue risk

If a government is not a direct sponsor of a project, it may still have a significant role in reducing risk for investors. One of the most important considerations for investors is electricity pricing, which needs to be efficient and rational.

The return that investors require to finance a project is primarily a function of the amount of risk they are required to assume. A clear funding stream (see Box 1: Funding versus financing above) is vital even where infrastructure is government-backed. An investor will not finance an infrastructure project unless long-term operations and maintenance costs can be met. There is clearly no shortage of private finance available. Instead, where financing is expensive or lacking, it is often due to a lack of clear funding streams, meaning that it is not possible for investors to be confident of how they will get their money back.

Nuclear power plants and other low-carbon electricity generation options have high fixed to variable cost ratios (i.e. they are capital intensive). High fixed costs represent a risk to investors because significant capital is spent or 'sunk' before first revenues are earned. Once built, the investment decision has been made, and there is limited scope to adapt to the prevailing market conditions at the time. In liberalised markets with high shares of variable renewable energy, reduced and highly volatile electricity prices create challenging conditions for investing in such assets without subsidy.

In order to secure affordable finance without subsidy, electricity price predictability is required to ensure that initial investment costs can be recouped over the life of a project. In regulated markets, such stability is provided by the regulation of the tariffs charged to customers. Absent of such stability, less capital intensive technologies may be favoured, even if their lifetime costs are higher. Securing competitive financing for nuclear power plants (as well as other low-carbon technologies) in deregulated markets is often therefore contingent on the use of mechanisms that, in effect, provide long-term stabilisation of electricity prices. A number of such measures have emerged, including power purchase agreements or 'PPAs', feed-in tariffs (FiTs), and contracts for difference (CfDs).

| Long-term contract | Description | Examples |

|---|---|---|

| Power purchase agreement (PPA) |

PPAs are the most widely used means of long-term revenue guarantee, and are used throughout the electricity industry. A PPA is an agreement between an electricity generator (the seller) and a purchaser (the buyer). The agreement stipulates the price and amount, as well as the term over which, the buyer purchases power from the seller. Buyers are typically wholesalers or similar that require secure supply at a fixed price (e.g. grid operators). PPAs may or may not be guaranteed by host governments. |

Akkuyu nuclear power plant, Turkey. PPA with Turkish power wholesaler, Tetas. Average price of 12.35 ¢/kWh for 15 years covering 70% of production from units 1&2 and 30% from 3&4. |

| Contract for difference (CfD) |

A CfD is a long-term contract between an operator and a counterparty, which might be a government company, set up to represent the interests of electricity customers. Under a CfD, the parties to the contract share the risk that the electricity price will not be sufficient to repay the capital expenditure over an agreed period. The difference between the ‘strike price’ (i.e. the cost of the project plus a margin to the operator) and the ‘reference price’ (i.e. the actual market price for electricity) is met either by the counterparty when the market price falls below the strike price or by the operator when the market price exceeds the strike price. The counterparty will recover the difference through a charge levied on electricity customers. If the market price exceeds the strike price, then the operator credits electricity customers with the difference. CfDs were introduced by the UK in 2014 as a means of supporting investment in low-carbon electricity generation projects. A CfD provides investors with a degree of revenue certainty and stability; but if market prices exceed the strike price, the counterpart to the CfD (i.e. customers) benefit. A CfD does not ‘reimburse’ the operator; rather, it resembles a hedging operation in the absence of a futures contract for a commodity. |

Hinkley Point C, UK. Strike price of £92.50/MWh (2012 prices). |

The CfD was introduced by the UK government to support investment in Hinkley Point C whilst avoiding direct government investment. Under the CfD, the investors retained all risks related to construction, protecting consumers from cost and schedule overruns. However, as a result, the cost of capital remained significant – about two-thirds of the overall cost. A duplicate plant at Sizewell in the UK reached final investment decision in July 2025. With the aim of reducing financing costs, and ultimate target of providing the benefits of the project to consumers at the lowest possible cost, it is being financed under a regulated asset base (RAB) model (see section below).

|

Box 2: Pricing a 'fair' CfD CfDs have the effect of transferring price-related risk from producers to consumers, by obligating the latter to guarantee shortfalls in market prices. Such mechanisms provide a hedge against future price changes for both parties. It is very difficult for investors to assume long-term electricity price risk when over two-thirds of capital is committed prior to first revenues. Such cost structures (i.e. high fixed to variable cost ratios) are shared by all low-carbon electricity technologies. Recent experience shows that in liberalised electricity markets, all low-carbon technologies require long-term price stabilisation to be investable. CfDs, like all long-term price guarantees, are not cost free. In agreeing to a fixed price contract to limit downside risk, both parties forego upside risk. For consumers, a new technology may emerge during the duration of the fixed price contract that can provide cheaper carbon-free energy; for producers, it is possible that future wholesale prices rise beyond the agreed contract value. These considerations require a judgement to be made about what constitutes a ‘fair’ CfD. It is the role of government to make that determination on behalf of citizens. Judged after the fact, a ‘fair’ CfD would provide insurance against upside and downside risk for investors in a symmetric manner. Set too high, a CfD could be construed as subsidy – allowing a producer to achieve revenue that would not be possible in a free market situation. Agreeing a ‘fair’ CfD value for a period of 30 years is extremely difficult. It is often assumed that current market prices provide a useful reference level. However, in many liberalised markets, wholesale prices correspond to short-run variable costs, and so are well below the average cost of producing electricity (which includes the plant investment cost). |

Encouraging investment: capping investor exposure

The capital intensity of nuclear power projects means the cost of capital has a strong bearing on the total generation cost. Reducing the risk perception of investors – and as a consequence, the risk premium charged by investors – can decrease the component of total costs that are related to finance.

Government involvement in a project usually makes it easier to raise low-cost debt finance. Lenders recognise that, as a last resort, loans are in effect backed by the state. Government involvement may be direct, in the traditional sense, where a project is financed from the public purse, a utility is in public ownership, or a government has a majority stake (see Government and corporate finance section above); or it may be indirect, for example financial assistance in the form of guarantees.

Loan guarantees

Governments may choose to back project promoters through the provision of loan guarantees. Typically these are extended to projects that are otherwise fully commercial arrangements between a plant’s owners and lenders.

Guarantees vary, but may provide lenders with assurance of full repayment including interest, or may simply protect a lender against a certain portion of potential losses.

Such loan guarantees have been used in the USA for the development of Vogtle 3&4, which commenced operation in April 2023 and March 2024 respectively.

Regulated asset base model

In the UK, where direct procurement by the government has been ruled out since the privatization of the electricity supply system, the Nuclear Energy (Financing) Act 2022 established a framework for financing nuclear power plants using a regulated asset base (RAB) model.

The RAB model is widely used for monopoly infrastructure in the UK, Australia and a number of other countries, but had not been widely used for electricity generation projects. It is generally used across multiple assets; the first time it was used to support a single asset construction project was the £4.2 billion Thames Tideway Tunnel sewage project in the UK, in 2016. Sizewell C, designated under the Act in November 2022, became the first power generation project in the UK to use the RAB model, reaching financial close in November 2025.

Under the Nuclear Energy (Financing) Act 2022, a nuclear developer receives a licence from an independent regulator following due diligence to confirm a proposed plant’s viability and value. The licence allows the developer/operator to pass costs onto its customers in exchange for the provision of the asset (and the supply of electricity from it). The charge, or the ‘allowable revenue’, is calculated based on a number of ‘building blocks’. The independent regulator sets the charges, ensuring that the developer can recover its costs plus a reasonable return on investment – and that the charges to users represent value for money.

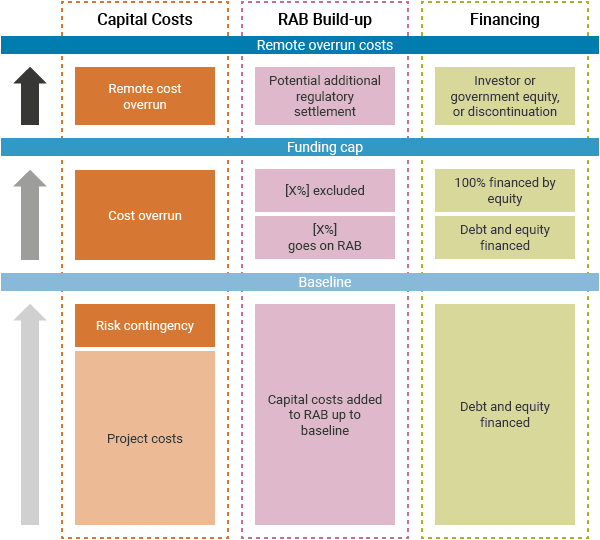

Building blocks of the nuclear RAB model

The RAB model allows costs to be recovered from users as construction proceeds

Source: UK government2.

* The weighted average cost of capital (WACC) represents the cost of financing the project.

A principal feature of the RAB model is that the independent regulator has a duty to ensure that the developer/operator can finance its activities. This provides bankable revenue in much the same way that a long-term contract (see above) does, reducing risk for investors, and reducing the cost of capital.

The RAB model also addresses the limitations of privatised utilities to finance multiple, very large capital investments from their balance sheets. Investing in a nuclear power plant may involve a period of 10 or more years of capital investment before first revenues. The RAB model in effect allows the capital outlay to be divided into steps. At each stage, the costs are agreed in advance, and subjected to scrutiny and efficiency tests by the regulator. Once approved, these costs would go into the RAB and could be recovered from users as construction proceeds. The opportunity to earn regulation-backed revenue during the construction phase of a project significantly changes the risk profile of the investment.

Under the RAB framework, the UK government underwrites the risk of construction cost overruns above a certain remote (i.e. unlikely to be reached) threshold. This ‘funding cap’ represents a sharing of risk between investors and customers. Up to a certain percentage, construction costs above the baseline (agreed at the time the RAB licence is granted), but below the funding cap, would be added to the RAB (i.e. paid for by customers), with the balance paid for by investors. For the remote risk of cost overrun beyond the funding cap, the government would have to either inject equity or terminate the project.

Risk sharing of baseline, funding cap and overrun costs

Above a certain remote threshold the UK government would underwrite the risk of construction cost overruns

Source: UK Government3

Aside from providing additional incentives to deliver the project within budget, the main function of the funding cap would be to limit the exposure of investors. This ‘enveloping’ of the investment lowers the risk profile considerably, opening up new categories of potential investors (e.g. pension and insurance funds), and allowing the cost of capital to be reduced materially.

Government-to-government financing and ECAs

Governments with strong domestic nuclear energy industries may seek to support export activities. As with domestic projects, support may be direct or indirect.

A state-owned utility may make an equity investment in a foreign project or support the project indirectly using an export credit agency (ECA). It is common for state-backed vendors to offer finance to support a project in which their technologies are being deployed. For example, China National Nuclear Corporation (CNNC) provided a loan of $9-10 billion to the Pakistan Atomic Energy Commission to build two ACP1000 reactors at the Karachi nuclear power plant. Where vendors are not state-backed, their balance sheets are likely to limit them to providing only part of the project’s financial requirements.

ECAs are used widely (not just for nuclear) and in effect provide a loan guarantee for a non-domestic project, reducing risk for other investors. ECAs are long-term financing debt instruments with competitive fixed interest rates, making them very attractive to exporting companies. It should be borne in mind that equipment manufacturers expect to be paid on delivery, successful commissioning and hand-over and will normally limit their liability for operational problems to the value of the equipment supplied.

The major official export credit agencies supporting nuclear energy projects are:

- Compagnie Française d'Assurance pour le Commerce Extérieur (Coface) was the French export credit agency until 2017, when its state export guarantee activities were transferred to Bpifrance Assurance Export. It has provided credits for Areva’s (now Framatome's) projects in China and Finland. Coface also guaranteed €570 million of loans raised by the Finnish utility TVO needed to finance the construction of the Olkiluoto 3 reactor built by Areva. TVO paid a market rate to Coface for the guarantee premium.

- Export Development Canada (EDC) is a self-funding state-owned enterprise. It provided finance to the Candu Qinshan III project in China.

- The Export-Import Bank of China (China Exim Bank) agreed in 2015 to loan Pakistan 85% of the cost of constructing the Karachi Coastal nuclear plant (about $6.5 billion) on concessional terms.

- The Export-Import Bank of Korea (Kexim) manages the government’s Economic Development Cooperation Fund. It provided finance worth $10 billion for the Barakah project in the United Arab Emirates out of $18.6 billion construction costs. The Korea Export Insurance Corporation (KEIC) provides insurance services.

- The Export-Import Bank of the United States (Ex-Im Bank), a government corporation that is not permitted to compete with private sector lenders, has extended finance worth $2 billion for the Barakah project in the United Arab Emirates at 3% interest (approximately), repayable over 27 years, to Westinghouse, CH2M Hill, Bechtel and another 20 smaller suppliers to support almost 2000 US jobs.

- Japan Bank for International Cooperation (JBIC) supports Japanese exporters with loans, loan guarantees and equity participation. Nippon Export and Investment Insurance (NEXI) is a provider of insurance services.

- The Swedish Export Credit Corporation (SEK) provided loan guarantees to Finnish utility TVO for the construction of the Olkiluoto 3 nuclear unit in view of the involvement of Swedish supplier Uddcomb, whose parent company is Areva (now Framatome). It is a state-owned corporation.

- The Bank for Development and Foreign Economic Affairs (VEB.RF, formerly Vnesheconombank) and its subsidiary, the Russian Agency for Export Credit and Investment Insurance (EXIAR), provide export finance and guarantees. It is funded by the Russian government and has a mandate to support and develop the Russian economy.

Guidelines developed by the Organisation for Economic Cooperation and Development (OECD) govern the manner in which export credits from government agencies can be used to fund nuclear export projects. These regulations are designed to create a 'level playing field' for all exporters. Under OECD rules, a maximum of 85% of the value of the export contract and costs occurring in the importing country for up to 15% of the value of the export contract are eligible for export credits. The balance of the foreign and local costs must come from commercial credit and owner’s equity. Terms for these loans are not to exceed 15 years.

Multilateral development banks

In the past, the World Bank, the European Investment Bank and a wide range of commercial lenders financed nuclear projects. The Development Bank of Latin America (CAF) supported the refurbishment and licence extension of Argentina's Embalse nuclear power plant in 2013. In June 2025, the World Bank ended its longstanding exclusion of nuclear power from financing, signing a partnership agreement with the IAEA to support the deployment of nuclear energy in developing countries. The Asian Development Bank similarly removed its exclusion of nuclear energy from its lending policy in November 2025.

Notes & references

Notes

a. The basic metric for any generating plant is the levelised cost of electricity (LCOE). It is the total cost to build, operate and decommission a power plant over its lifetime divided by the total electricity output dispatched from the plant, hence typically cost per megawatt hour. It takes into account the financing costs of the capital component (not just the 'overnight' cost). [Back]

References

1. OECD Nuclear Energy Agency, Projected Costs of Generating Electricity, 2015 Edition (September 2015) [Back]

2. UK Government, Department for Business, Energy & Industrial Strategy, Consultation on a Regulated Asset Base (RAB) Model for Nuclear (July 2019) [Back]

3. ibid. [Back]

General sources

Hugo Lidbetter, SMRs and RABs – Acronyms that spell the future of new nuclear in the UK?, Fieldfisher (25 July 2019)

Dieter Helm, The Nuclear RAB Model (12 June 2018)

International Atomic Energy Agency, Managing the Financial Risk Associated with the Financing of New Nuclear Power Plant Projects, IAEA Nuclear Energy Series No. NG-T-4.6 (July 2017)

International Atomic Energy Agency, Financing Nuclear Power in Evolving Electricity Markets (April 2018)

OECD Nuclear Energy Agency, The Financing of Nuclear Power Plants (2009)

Related information

Economics of Nuclear PowerNuclear Power in the World Today